What we’re learning along the way

From challenge to change

What we’re learning along the way

To flourish in a T+1 ecosystem, our data clearly shows that greater automation, earlier instruction matching, and better cross-time zone coordination will be needed.

How the industry got T+1 over the finish line in North America

The Capital Markets industry did a lot of heavy lifting to get ready for T+1 in North America, and the hard work has paid off.

Ahead of T+1, industry-wide efforts were made to prepare and educate market participants about the changes and their impact on the securities ecosystem. As a result, firms had plenty of time to invest in headcount, test their systems, and make the necessary technology upgrades ahead of the North American transition.

Reflecting these trends, we also spotted a sharp fall in cancellation messages post-T+1 and increased volumes of MT 578, i.e. allegement messages and pre-advice messages. Our data shows a 16% increase in MT 578 allegement messages and a 20% jump in MT 54x instruction as pre-advice messages.

These trends suggest improved certainty and readiness in instruction workflows across the market.

What's next?

The transition to T+1 in North America has largely been successful. However, challenges remain, particularly for participants operating across distant time zones.

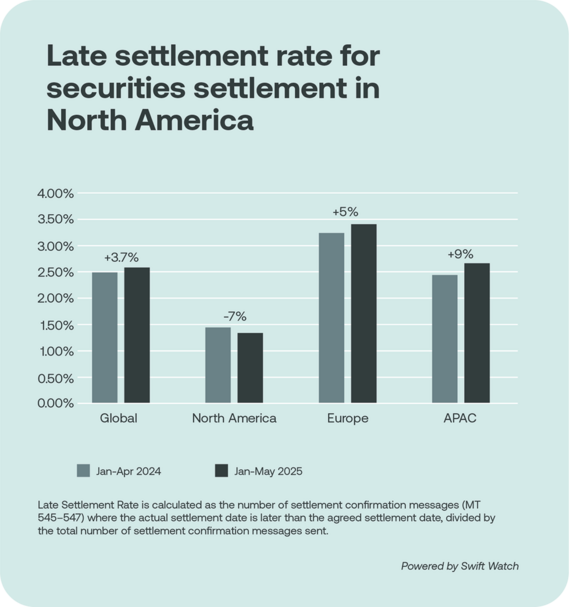

Overall, global late settlement rates increased marginally (+3.7%), while pre-T+1 late settlement rates were at 2.49%. A year later, they are at 2.58%, showing very little change.

However, the picture varies by region.

|

Asia Pacific APAC-based instructing parties saw a 9% increase in late settlement rates when settling into North America, highlighting the persistent impact of time zone constraints and liquidity cut-offs. |

Europe Instructing parties in Europe also experienced growing friction (+5%). |

North America North America-based actors saw a 7% improvement, likely benefiting from proximity and mature affirmation workflows. |

To understand why these frictions persist, we analysed MT 548 messages—particularly those flagged as unmatched (UMAT) or failed (PENF):

- Unmatched instructions typically stem from mismatched trade data, incorrect safekeeping account details, or discrepancies in settlement amounts.

- Settlement fails are most often due to a lack of securities, instruction delays, or cash/credit shortfalls. While manual processing still contributes to inefficiencies, many of these issues reflect broader operational gaps. These include fragmented trade data, tight funding windows, or a lack of readiness for same-day instruction. Solving these issues will require more than automation; it demands better coordination across systems, earlier affirmation, and shared visibility across the post-trade chain.

Manual processing is still an obstacle

An analysis of Swift MT 548 messages picked up on several lingering pain points, post-T+1. This analysis is based on MT 548 messages flagged with status codes UMAT and PENF and their reason codes, Jan-May 2025.

An ongoing reliance on manual processing appears to be a root cause of many of these problems, especially for firms who are not Swift users. This is also underlined by a recent Value Exchange study, which found that 51% of post-T+1 exceptions are still resolved manually through emails or phone calls.

The challenge is particularly acute among smaller and less automated institutions.