Payment Optimisation Playbook

Cross-border payments are evolving rapidly, yet persistent structural frictions continue to slow processing, increase cost and reduce transparency, particularly at the final stage of a transaction.

Understanding where these frictions occur is critical to improving payment speed and delivering a more consistent customer experience.

Payment Optimisation Playbook

75% of payments travelling over our network reach beneficiary banks within just 10 minutes. This progress - aligned to the G20 goals for cross-border payments - reflects a sustained investment in infrastructure, standards and connectivity.

However, the ‘last mile’ - where funds are processed, validated and credited to the beneficiary - accounts for around 80% of total processing time, making it the greatest opportunity for improving the customer experience.

Introduction

Cross-border payments sit at the heart of global finance. Significant progress has been made in recent years, with improvements in infrastructure, interoperability and data standards helping to reduce processing times across many markets.

Yet progress remains uneven. While payments increasingly reach destination banks within minutes, delays can still occur before funds are credited to the recipient's account. These frictions affect not only speed, but also transparency, cost and access to services.

Introducing the Payment Optimisation Index and Playbook

To help the industry better understand and address these frictions, Swift has developed the Payment Optimisation Index and Playbook. Together, they provide a data-driven view of where delays occur and practical guidance on how to improve payment performance.

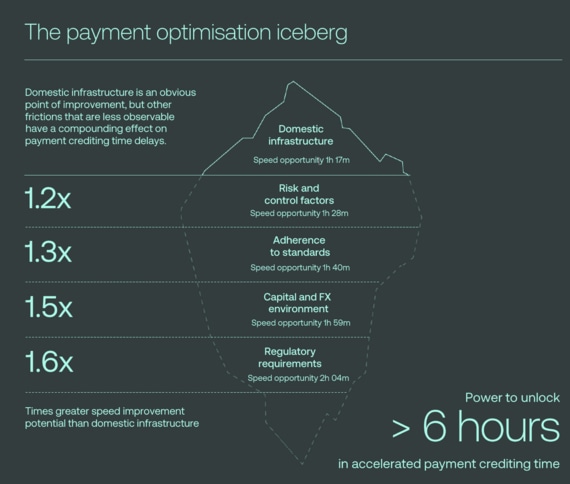

The Payment Optimisation Index provides a global benchmark that measures how different types of structural friction influence payment crediting time. It groups these conditions into five key categories and connects them to measurable contributing factors, enabling direct comparison across markets.

By analysing both quantitative data and qualitative insights, the Payment Optimisation Index identifies where delays originate and which frictions have the strongest impact on performance. This provides an empirical foundation for prioritising actions that can improve payment outcomes, particularly in the last mile.

The Payment Optimisation Playbook then combines these quantitative insights with market analysis to identify practical priorities and clear next steps for different stakeholder groups across the payments ecosystem.

Together, these are designed to help policymakers, market infrastructures, financial institutions and technology providers prioritise action and accelerate progress towards faster, more efficient cross-border payments.

Deep dive into friction categories

The Payment Optimisation Paybook explores five categories of structural friction that influence how cross-border payments are processed and credited.

Each reflects underlying market conditions and has a measurable impact on payment speed, particularly at the beneficiary crediting stage.

From insight to action

Taken together, these frictions highlight that there is no single constraint shaping cross-border payment performance. Instead, delays emerge from the interaction of multiple factors, which vary across markets and corridors.

The Payment Optimisation Playbook demonstrates that the greatest improvements in payment speed often come from addressing frictions that sit above the underlying payment rails. Strengthening regulatory clarity, improving data quality, aligning standards and enhancing coordination can deliver measurable gains without requiring large-scale infrastructure change.

Accelerating progress will require coordinated action across the ecosystem. Policymakers, financial institutions, market infrastructures and technology providers all play a role in aligning practices, improving interoperability and ensuring that controls support efficient processing.

By focusing on the areas with the greatest impact, the industry can make meaningful progress towards the G20 goals for enhancing cross-border payments and deliver faster, more transparent and more predictable cross-border payments.

Appendix

The appendix provides the supporting detail behind the analysis, including definitions, data sources and methodology.

It outlines how the Index is constructed, how contributing factors are measured and how results are interpreted, ensuring transparency and consistency across markets.

Payment Optimisation Playbook

A targeted analysis and guide to tackling structural frictions in cross-border payments